[DRAFT, WORKING DOCUMENT]

Latest update: 19th July 2015

[Image above is of the chin of the current head of the International Monetary Fund]

The Greek government is struggling to pay the debts it took on to bail out the country's private banks. The newly elected government, headed by Prime Minister Alexis Tsipras, has been opposing IMF, EC and ECB 'bailout' conditions on humanitarian grounds. On 5th July 2015, a large majority (61%) of Greek citizens who voted on a referendum on this issues opted to reject the bailout terms offered by this 'Troika'.

Demands placed on the Greek government included implementing a higher tax on goods and services, forcing 100% advance tax payments on corporations and generally increasing taxes across the board. Social welfare entitlements were to be limited and payments decreased. More effective measures were required to target tax evasion. The electricity company, the airport and shipping ports were to be privatised, efforts were required to weaken the collective bargaining of workers And so on. [1]

However, only days after the Greek people took Tsipras' lead to reject such imposed austerity in the referendum, the Greek Prime Minister took a U turn and signed up such measures after all. [2]

“Alexis Tsipras at some point decided that his government, our government, was at gunpoint. We were given a choice between being executed and capitulating and he decided that capitulation was the optimal strategy."Said Greece's former Finance Minister, Yaris Varoufakis. [3]

About one third of Tsipras party have voted against the austerity measures. They want Greece to reintroduce it's national currency, the drachma. [4]

But what made Greece such a debt junkie in the first instance? Does Greece suffer from a fundamental lack of economic capacity? Is Greece exceptional with regard to her inability to repay? Have lenders inappropriately pushed loans? Have the recipients borrowed beyond their means?

In 2012, Greece's government had the largest sovereign debt default in history and on 30th June, 2015, Greece became the first developed country to fail to make an IMF loan repayment.[5]

Events are unfolding that reveal that most of Greece's struggle and dilemma is revealed to be symptomatic of a much wider and global, form of economic and financial failure.

The former Greek finance minister, Yanis Varoufakis resigned months after taking office in early 2015. He has pleaded with his nation's creditors that Greece is simply not capable of paying back the debt. He is alarmed that the so-called 'Troika' of the IMF, the European Commission and the European Central Bank are not 'bailing out' Greece, as they publicly assert. Rather, Greece is being loaded with more debt. Greece says Varoufakis, is "caught up in an existentialist crisis caused by its membership of a problematic currency union."[6]

Varoufakis explains the dynamics of Greece's extraordinary bailout process:

- "Step 1: Banks issued private bonds which they did not intend to sell to anyone

- Step 2: Banks got (under a veil of ignorance and a conspiracy of silence) the Greek state to guarantee these bonds – without seeking parliamentary approval, without the troika’s official approval, without even informing the electorates in Greece or in Germany or anywhere else of this massive increase in the Greek state’s effective liabilities

- Step 3: Banks then posted these bonds with the ECB in exchange of instant cash." [7]

At the same time, Greece is being weakened in its capacity to repay this rather dubious form of debt by demands for greater and greater fiscal austerity. Varoufakis calls it 'ponzi austerity' where every effort is made to give the public the illusion that the debt problem is being dealt with whilst the reality is that this problem has actually worsened.

"When bankrupt a large loan does not help, as long as the loan is not preceded by a debt write off. And, when the large loan, without an upfront haircut, comes with the condition of reducing your income (for this is what austerity does), then it is a predatory, toxic, ridiculously irrational policy."[8]

The vast portion of the capital said to have been passed to Greece is, Varoufakis said, being used to prop up large German and French banks in particular.

The crisis in Greece began to climax shortly after the beginning of a global financial crisis which was officially declared to have begun in 2008. Before that most citizens in the richest industrial countries might have believed we were still enjoying one of history's longest and greatest economic booms. For instance, in 2005 the US Federal Reserve chairman Ben Bernanke spoke of a 'global savings glut'.

In actuality a form of 'ponzi growth' was taking place in the world economy.

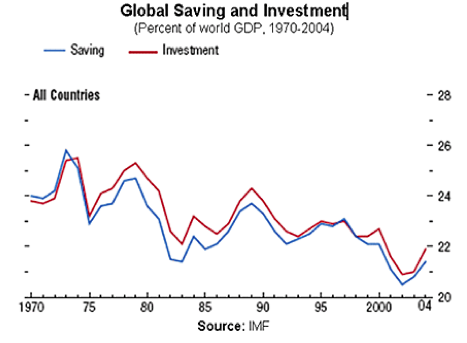

"...we observe is that world savings rates have actually declined from the 1970’s to the present time [See above chart]. So the crude notion of a savings glut doesn’t seem to reconcile the data with the theory because if there is a savings glut now then there would have been a much higher savings glut in the 1970’s, and yet real and nominal rates were high in the late 1970’s and extremely high in the early 1980’s. Ironically, the savings glut concept, global aggregate demand shortfall, insufficient consumption discussions dominated the economic discussions of the 1930’s." [9]

In an extremely unbalanced global trading regime, North America' economy was acting as the world's 'consumer of last resort'. Nations with a balance of trade surplus were flooding their capital mostly into the US to retain foreign exchange parity with the US dollar. This supported the US' budget and current account deficits which, in turn, kept the global reserve currency (the US dollar) strong. Clearly the situation was unsustainable as America's deficits in its current account, trade and fiscal balances were growing out of proportion to its real economic capacity.

A senior Australian Reserve Bank official observing this dynamic said it was "akin to

the Dotcom Crash "… and were it to stop, a sharp fall in the US dollar and a bond market sell-off would occur, pushing up US and world interest rates in a global economic crash. This would hit US economic growth and thereby cut Chinese exports of manufactured goods to the American market (undermining the engine of global growth)." [10]

Major trade imbalances were being compensated for by equal and opposite capital imbalances. The surplus countries (Japan, Germany, China...) must finance the deficit country (the US, Greece, Ireland, Portugal, Spain...) and this financing maintains its internal demand and the external demand of the surplus country. [11] Stability is maintained as long as household income in the deficit country parallels or exceeds household acquisition of debt. In the US household debt began to outstrip earnings from the late 1990s. [12]

When international lenders begin to fear the repayments of debt may not be realised, or for other reasons, capital flows out of the fragile periphery countries and throws them into economic turmoil. This is how the Greek finance minister described the unravelling in Greece once the global financial crisis commenced:

"...The reason for our insolvency was simple: The Eurozone was incapable of absorbing the shockwaves of the 2008 global earthquake. Once the capital inflows that had flooded the Periphery went out like a vicious tide, they left behind nothing but weedy posts and marooned public and private sectors. Unable to reduce the international value of our countries’ debts and banking losses through currency depreciation, with states that lacked a central bank to have their back, and a central back without a state to have its back, Europe’s mountain of debts was bound to rise while incomes took a hit. The definition of bankruptcy writ large." [13]

...

.... to be continued...

REFERENCES and NOTES:

[1] Table 1. Greece: Prior Actions

Policy:

Actions to be taken in consultation with EC/ECB/IMF staff

http://europa.eu/rapid/attachment/IP-15-5270/en/List%20of%20prior%20actions%20-%20version%20of%2026%20June%2020%2000.pdf

[2] Greek bailout: Europe strikes deal after marathon talks

Mark Thompson. 12th July 2015

http://money.cnn.com/2015/07/12/news/economy/greece-bailout-europe-conditions/

[3] Greek debt crisis: reforms will fail, says ex-finance minister Yanis Varoufakis

Jamie Grierson and Helena Smith

Sunday 19 July 2015 00.17 AEST

http://www.theguardian.com/world/2015/jul/18/greece-debt-crisis-reforms-fail-yanis-varoufakis

[4] Says Anna Asimakopoulou, an MP with the conservative New Democracy party in Greece.

Source: Now a deal has been done, what lies ahead for the Greek economy? Helena Smith in Athens. The Observer, 19th July 2015.

http://www.theguardian.com/world/2015/jul/18/greece-eu-debt-deal-what-lies-ahead

[5] Greece fails to make IMF payment as bailout expires

Elena Becatoros and Raf Casert, The Associated Press

Published Tuesday, June 30, 2015 5:02AM EDT

http://www.ctvnews.ca/business/greece-fails-to-make-imf-payment-as-bailout-expires-1.2446852

[6] Yanis Varoufakis: Italy’s collapse will change the Austerian way in Europe

Interview by Jorge Nascimento Rodrigues. 25th June 2013

http://janelanaweb.com/novidades/yanis-varoufakis-italys-collapse-will-change-the-austerian-way-in-europe/

[7] How the Greek Banks Secured an Additional, Hidden €41 billion Bailout from European taxpayers

Posted on May 11, 2014 by yanisv

Yanis Varoufakis – Thoughts for the post 2008 world

http://yanisvaroufakis.eu/2014/05/11/how-the-greek-banks-secured-an-additional-hidden-e41-billion-bailout-from-european-taxpayers/

[8] Yanis Varoufakis: Italy’s collapse will change the Austerian way in Europe

Interview by Jorge Nascimento Rodrigues. 25th June 2013

http://janelanaweb.com/novidades/yanis-varoufakis-italys-collapse-will-change-the-austerian-way-in-europe/

[9] Spotlight, February 2006.Chris Dialynas Discusses the Causes and Implications of Low Interest Rates and the Yield Curve Conundrum.

Chris P. Dialynas, Managing Director, Portfolio Manager and Senior Member of PIMCO’s Investment Strategy Group

http://australia.pimco.com/LeftNav/PIMCO+Group+Spotlight/2006/Dialynas+Spotlight+Feb+2006.htm

[10]

The Generation Project: 2000-2005

© Mark Verma 2005

http://members.iinet.net.au/~verma/p_generation11.html

[11] If this financing is by buying assets, the surplus country gains the “property” of the deficit country; and if the financing is by loans, the surplus country gains “sovereignty” over the deficit country.

[12]

Guest

Post: Our Era’s Definitive Dynamic: Diminishing Returns

Submitted

by Tyler Durden on

11/09/2013 20:59 -0400

Submitted

by Charles Hugh-Smith via Peak Prosperity