I found this definition of 'capital' on the web tonight:

"wealth

in the form of money or other assets owned by a person or organization

or available for a purpose such as starting a company or investing."

[Where 'investment' is defined as "the action or process of investing

money for profit."]

Which effectively makes 'capital' a function of (monetary)'demand' and the profit motive.

I'd settle for wealth and abundance and forget the rest.

"Whoever

loves money will never have enough money. Whoever loves luxury will not

be content with abundance. This also is pointless."

Ecclesiastes 5:10

Monday, May 9, 2016

Friday, January 29, 2016

A Theory Explaining Why Severe Weather is Occurring

Global warming is slowing the gulf stream system, also known as the Atlantic Meridional Overturning Circulation (AMOC). The AMOC is a gigantic ocean system that’s driven by differences in temperature and the salinity of sea water. Ocean temperatures off the U.S. east coast are warming faster than global average temperatures and there’s a “cold blob” in the subpolar Atlantic understood to be sourced from Greenland ice-melt water. These latter two features are regarded (by some scientists) as a characteristic response to a warmer world. The slowdown of the AMOC is in turn, a result of the ocean freshening at high latitudes due to these large infusions of meltwater from Greenland resulting in a cooling in the North Atlantic region, as less ocean heat reaches the region — aka, the “blob.”. The far North Atlantic waters are being diluted by the Greenland melt waters and are no longer salty enough. Therefore the waters don’t sink as much, and this slows (or may even eventually shut down the AMOC circulation. The AMOC global conveyor has been weakening, by the way, since the late 1930s. The slowing of the Gulf Steam System/AMOC should drive faster sea level rise on the East Coast where sea level rise for a 600-mile-long “hotspot” along the East Coast (north of Cape Hatteras) has already been measured at “3-4 times higher than global average”. A 2015 discussion paper by some of the world’s leading climatologists argues that “Shutdown or substantial slowdown of the AMOC, besides possibly contributing to extreme end-Eemian (brief? sea level) events, will cause a more general increase of severe weather.”

REFERENCES:

(i) The surprising way that climate change could

worsen East Coast blizzards

By

Chris Mooney January 25, 2016

https://www.washingtonpost.com/news/energy-environment/wp/2016/01/25/climate-scientist-why-a-changing-ocean-circulation-could-worsen-east-coast-blizzards/?postshare=1471453766419405&tid=ss_tw

(ii)

Recent

studies from the National Oceanic and Atmospheric Administration found that

ocean temperatures off the U.S. East Coast are expected to warm three times

faster than the global average. The warming coincides with increased C02

emissions.

(iii)

Stefan Rahmstorf of the Potsdam Institute for Climate Impact

Research, an expert on the Atlantic circulation phenomenon known by the

technical name meridional

overturning circulation, or AMOC.

(iv)

The Greenland melt. Eric Steig. 23

January 2013.

http://www.realclimate.org/index.php/archives/2013/01/the-greenland-melt/

(v)

Is Climate Change Supercharging Storms Like Jonas And Sandy More Than We

Thought? by Joe Romm Jan

25, 2016 4:41 pm

http://thinkprogress.org/climate/2016/01/25/3742321/climate-change-jonas-sandy/

(vi)

Blizzard Jonas and the slowdown of the Gulf Stream System.

Stefan. 24 January 2016

http://www.realclimate.org/index.php/archives/2016/01/blizzard-jonas-and-the-slowdown-of-the-gulf-stream-system/

Thursday, December 17, 2015

Is America's Freedom Unhinged From Reality or Truth?

Economic historian, Dr. Rupert Ederer issued an urgent warning to America and other nations who had adopted the neo-liberal ethic. In October 2012 in his article "America and Catholic Social Teaching: An Urgent Warning". He wrote:

Leo XIII [his encyclical 'Rerum Novarum' and his important encyclical On Human Liberty (Libertas Praestantissimum) which came out in 1888.]

Ederer concludes his article by pointing out that the present Pope Benedict XVI's encyclical 'Cartitas in Veritate' "addressed precisely the quintessential link between charity and truth.

"Serious study of Caritas in Veritate" says Ederer "not to mention widespread implementation of that principle, has scarcely begun."

"Capitalist plutocracies should be forewarned. They may well be facing some kind of parallel to the heinous outburst known as the French Revolution. That followed prolonged abuse of political power by long-standing hereditary monarchies and their associated aristocracies. The current murmur of revolution stems from the abuse of economic power by a class of capitalistic plutocrats nurtured in recent centuries by a cult of freedom which has come to be known as liberalism. Basically that is about freedom unhinged from reality — or truth." [This is] "Indicated in the Catholic Church’s social teachings from the start....the failure of the economic liberals, and now neoliberals, to observe “in the area of economic and social activity” the important link between the “truth about man.” That shortcoming gave birth to Marxian socialism, and now to the current and fatal capitalistic economic pandemonium."Ederer invokes the stated concerns and even outright opposition of a long series of leading Catholic world figures over the way the neoliberal ideological movement first took hold and then became firmly entrenched:

- the present Pope Benedict XVI [encyclical, 'Caritas in Veritate']

- Pope John Paul II in January 1999 and his 'Laborem Exercens', 'Sollicitudo Rei Socialis' and 'Centesimus Annus

- Pope Paul VI [May 1971 'Populorum Progressio']

- Pope John XXIII [1961 encyclical 'Mater et Magistra']

- Monsignor Fulton J. Sheen ['Communism and the Conscience of the West' (1948)]

- Pope Pius XII [Address to Italian Workers, June 1941]

- Pope Pius XI in 1931 [encyclical Quadragesimo Anno]

- Father Heinrich Pesch, Jesuit Master Economist [Lehrbuch der Nationalökonomie (1923)]

"People, not excluding learned economists, tend to lapse all too easily into extremes. The recklessness in socialistic free labor union policy did evoke and continues to evoke reaction, so that today one feels entitled to talk about a kind of ‘neo-Manchesterism.’ Mises is regarded as the main exponent of this trend, and because of his incisive and original criticism of socialism he has also gained acceptance and respect among authors who, unlike him, have stepped forward and supported the legal protection of women and children, and social insurance of workers. Mises is on the wrong track when he attributes the terrible conditions in English factory regions where Manchesterism prevailed, not to that phenomenon, but to other circumstances. The historical development of industry among the various nations, and also a proper understanding of human nature, pass judgment on individualistic freedom."Also mentioned are earlier Catholic popes who laid the foundation for the Church's social teachings on the economic order and the institution's opposition to economic liberalism:

Leo XIII [his encyclical 'Rerum Novarum' and his important encyclical On Human Liberty (Libertas Praestantissimum) which came out in 1888.]

Ederer concludes his article by pointing out that the present Pope Benedict XVI's encyclical 'Cartitas in Veritate' "addressed precisely the quintessential link between charity and truth.

"Serious study of Caritas in Veritate" says Ederer "not to mention widespread implementation of that principle, has scarcely begun."

Wednesday, March 18, 2015

Do we all share the same future as Greece?

DRAFT, WORKING DOCUMENT

A psychotic dynamic plays out

Headlines today often refer to the phenomenon of the 'bankrupt nation'. It's a jarring mental abstraction. A pure accounting term is being applied to civil society and the complex web of economic activities of a people who exist within any particular national boundary. The spectre of wages being cut in half, public servants being laid off en-masse, interest rates on housing and business loans climbing through the roof, children going hungry, etc.

On the other hand, an incredible juxtaposition is revealed as private banks, whilst in reality being functionally bankrupt, are 'bailed out' by the very societies now described as insolvent!

Such a form of global psychotic dynamic would prompt a reasonable observer to try to find out what is really going on? Clearly sources of international finance have become much more important than either the viability of national economies and the lives of people who live within them. How did this extraordinary situation occur?

Nations on the global periphery - the 'subprimers' - are being loaded with more and more debt

Citizens of nations such as Greece, Ireland, Portugal and Spain, those that tend to be on the global economic 'periphery' are subject to deep austerity measures as greater and greater levels of debt are being loaded onto their governments's respective 'balance sheets'. Why this is happening is a long story that is difficult to articulate. Much evidence points to a playing out of the inherent defects of the social relations inherent in global capitalism itself. The functional structure of our exchange relationships have been rigidified into patterns of practice and thought that largely benefit a small global elite (whilst threatening the biosphere that ultimately sustains us). Our lives have become organised around the artificial creation of wants. Production is defended as satisfying those wants and production, in turn, creates wants. As JK Galbraith warned decades ago, the more amply an individual is supplied the less urgent is the need for such goods, with longer term implications about the sustainability of demand for such goods. A 'squirrel wheel' of want creation and production for wants - all justified on the basis of the creation of jobs - has been promoted whilst many fundamental human and environmental needs are still largely dismissed. [1]

As the 'squirrel wheel' turns on the global scene nations get to be either creditors (with a trade surplus) or debtors until this game of monopoly comes to its predictable conclusion. The ultimate demise of export-dependent economies, like Germany for instance, is that purchasing power dries up in the trade-deficit nations that Germany sells to. Those countries, then, can no longer buy Germany's exports. Whatever happens after that point is reached losses will probably be forced on both sides. The burden of debt is simply too great.

Financialisation

In the 1980s a process of 'financialisation' in the world economy stepped up. Satyajit Das, an Australian former banker, and current author and academic explains that over the last several decades economic growth "has been based increasingly on rising borrowings and financial rather than real engineering. There was reliance on debt-driven consumption. It resulted in global trade and investment imbalances, such as that between China and the US or Germany and the rest of Europe." [2]. However strong evidence points to these imbalances being mirrored in the unequal world distribution of key and vital resources such as oil in the first instance.

Even as early as 1964 - the year world oil discoveries peaked - the global market for securities (the Euromarket) grew immensely from around this time. Huge sums of unregulated short term capital began to flow in and out of national boundaries without effective constraints. A destabilisation of the values of currencies occurred around the world as a consequence.

Historically, then, the rise of global debt could be seen to be linked to the inability to increase the amount of oil available per head of population since the late 1970s.

"Per capita world oil consumption has remained remarkably constant at an average 4.54 barrels per capita (Standard Deviation = 0.10) for the 27 years inclusive from 1983-2009." [3]

It is not surprising that, coinciding with the beginning of this long-term energy plateau, there was a reversal in the ratio of US savings to investment.

"Up till 1980 [4], US investment was financed from internal savings, which always exceeded investment. This reversed in 1980 and savings from then on fell behind investment." [4]

Henry CK Liu explained how the new high energy prices that emerged around 2005 create new economic norms that might explain this dichotomy of stagnating energy availability and limited social savings. Liu said that "the same material quantity in transactions simply involves greater cash flow. Therefore nominal GDP is seen to rise whilst the real economy actually stagnates. Liu said that no interest rate policy is capable of containing inflation from higher energy prices. Economic bubbles form, whilst profit is shifted to different sectors.

"High energy prices translate into reduced consumption. There may be no increased productivity. Workers may simply work longer hours."[6]

'An Age of Discontinuity'

Some two decades late, in 1982, an Australian politician, Barry Jones, published a book [7] with the intent of alerting people to 'An Age of Discontinuity' - 'a post-industrial era' that had begun. Jones said that forces at play such as oil and general resource depletion, sharply escalating world population growth, local scarcities, great technological change, consumer society, etc had created a situation where nations experienced much greater international interdependency in order to function. The influence and power of national governments had greatly reduced whilst mobile transnational corporations were taking advantage of new technological and arbitrage opportunities for cheaper labour, finance and resources 'somewhere else'.

Mr Jones most emphasised in his book 'Sleepers Wake' the new and capital/energy intensive technologies that emerged in the 1970s and 1980s. They had become 'labour-displacing' rather than 'labour-complementing' in their nature. As a result manufacturing no longer existed as a dominant employer with many countries then in the process of 'de-industrialising' and moving to largely service-based economies instead. But service jobs were also being replaced by computerisation and modern telecommunications technologies.

Human services, of course, are an essential component of any economic system. A formal service-based economy, however, depends upon the reliable and ample flow of the basic and essential provisions of life, such as food and energy. If they have to be imported national purchasing power is necessary. On the other hand, energy producers need a minimum price to sustain production levels; and that minimum price needs to grow as energy-intense fuels get harder and harder to reach.

It's not surprising that, in this context. investment became sourced through other means such as debt, downsizing, greater productivity, taking shortcuts through deregulation and other forms. Rent seeking became increasingly dominant.

How, then, are we to continue life on a consumption-based 'squirrel wheel' in a world where there are not only fewer paid jobs, but a sharply decreasing resource base to sustain them? How are nations to obtain adequate levels of foreign exchange to sustain an industrial economy? In the final chapter Jones posed a generic and thoughtful (if partial) solution:

"Redefine work as 'any form of activity or time use that is or may be beneficial to society and/or to the person performing it'. Income should be re-defined to include 'acknowledgement of the right to receive economic support' in addition to 'reward for work done'.

At present our incomes are shrinking and the global financial system, as we've known it, is falling apart. How, then, are national governments going to provide real incomes (real purchasing power) to its displaced industrial workers in the post-industrial context. In this, our crisis epoch?

Without dramatic change in our financial institutions and in our daily patterns of belief and action, Jones' solution sounds like another way to simply perpetuate a state of bankruptcy. Sustainability requires the reversibility of dire global trends, not an adaptation to them.

REFERENCES:

[1] John Kenneth Galbraith 'The Affluent Society' (first published 1958). Pelican Book Paperback. Page 149, 153.

[2] Why we need to lie to ourselves about the state of the economy

Satyajit Das August 28, 2015

http://www.smh.com.au/comment/satyajit-das-column-20150825-gj7bcy.html

[3] World Per Capita Oil Consumption 1965 – 2009 (pdf/3 pages) by John H. Walsh.

http://pages.ca.inter.net/~jhwalsh/oilcapv3pages.pdf

[4] Figure 2 in Alan Cole's article: 'Losing the Future: The Decline of U.S. Saving and Investment' dated October 01, 2014, shows that investment rose above savings earlier than 1980. This rise in 'investment' funds was likely the result of the 9 fold increase in oil prices that occurred in the 1970s.

http://taxfoundation.org/article/losing-future-decline-us-saving-and-investment

[5] The new world order and the failure of globalisation

Alan Freeman (2002): The new world order and the failure of globalisation. Unpublished.

The new political geography of poverty. University of Greenwich

http://mpra.ub.uni-muenchen.de/2652/

Posted on 10th April 2007

[6] The real problems with $50 oil

By Henry C K Liu May 26, 2005

http://www.atimes.com/atimes/Global_Economy/GE26Dj02.html

[7] 'Sleepers Wake - Technology and the future of work', Barry Jones. Oxford University Press 1982.

[8] Charles Derber in his 1998 book 'Corporation Nation' quotes former US President Rutherford B Hayes about the 'Gilded Age' he lived in: "This is government of the people, by the people and for the people no longer. It is a government of corporations, by corporations and for corporations." Derber observes of our contemporary reality "[Corporations "constant dialogue] is more than idle chatter: their intricate network of connections constitutes what is, in essence, a new worldwide corporate web." Page 18.

Historically, then, the rise of global debt could be seen to be linked to the inability to increase the amount of oil available per head of population since the late 1970s.

"Per capita world oil consumption has remained remarkably constant at an average 4.54 barrels per capita (Standard Deviation = 0.10) for the 27 years inclusive from 1983-2009." [3]

It is not surprising that, coinciding with the beginning of this long-term energy plateau, there was a reversal in the ratio of US savings to investment.

"Up till 1980 [4], US investment was financed from internal savings, which always exceeded investment. This reversed in 1980 and savings from then on fell behind investment." [4]

Henry CK Liu explained how the new high energy prices that emerged around 2005 create new economic norms that might explain this dichotomy of stagnating energy availability and limited social savings. Liu said that "the same material quantity in transactions simply involves greater cash flow. Therefore nominal GDP is seen to rise whilst the real economy actually stagnates. Liu said that no interest rate policy is capable of containing inflation from higher energy prices. Economic bubbles form, whilst profit is shifted to different sectors.

"High energy prices translate into reduced consumption. There may be no increased productivity. Workers may simply work longer hours."[6]

'An Age of Discontinuity'

Some two decades late, in 1982, an Australian politician, Barry Jones, published a book [7] with the intent of alerting people to 'An Age of Discontinuity' - 'a post-industrial era' that had begun. Jones said that forces at play such as oil and general resource depletion, sharply escalating world population growth, local scarcities, great technological change, consumer society, etc had created a situation where nations experienced much greater international interdependency in order to function. The influence and power of national governments had greatly reduced whilst mobile transnational corporations were taking advantage of new technological and arbitrage opportunities for cheaper labour, finance and resources 'somewhere else'.

Mr Jones most emphasised in his book 'Sleepers Wake' the new and capital/energy intensive technologies that emerged in the 1970s and 1980s. They had become 'labour-displacing' rather than 'labour-complementing' in their nature. As a result manufacturing no longer existed as a dominant employer with many countries then in the process of 'de-industrialising' and moving to largely service-based economies instead. But service jobs were also being replaced by computerisation and modern telecommunications technologies.

Human services, of course, are an essential component of any economic system. A formal service-based economy, however, depends upon the reliable and ample flow of the basic and essential provisions of life, such as food and energy. If they have to be imported national purchasing power is necessary. On the other hand, energy producers need a minimum price to sustain production levels; and that minimum price needs to grow as energy-intense fuels get harder and harder to reach.

It's not surprising that, in this context. investment became sourced through other means such as debt, downsizing, greater productivity, taking shortcuts through deregulation and other forms. Rent seeking became increasingly dominant.

How, then, are we to continue life on a consumption-based 'squirrel wheel' in a world where there are not only fewer paid jobs, but a sharply decreasing resource base to sustain them? How are nations to obtain adequate levels of foreign exchange to sustain an industrial economy? In the final chapter Jones posed a generic and thoughtful (if partial) solution:

"Redefine work as 'any form of activity or time use that is or may be beneficial to society and/or to the person performing it'. Income should be re-defined to include 'acknowledgement of the right to receive economic support' in addition to 'reward for work done'.

At present our incomes are shrinking and the global financial system, as we've known it, is falling apart. How, then, are national governments going to provide real incomes (real purchasing power) to its displaced industrial workers in the post-industrial context. In this, our crisis epoch?

Without dramatic change in our financial institutions and in our daily patterns of belief and action, Jones' solution sounds like another way to simply perpetuate a state of bankruptcy. Sustainability requires the reversibility of dire global trends, not an adaptation to them.

REFERENCES:

[1] John Kenneth Galbraith 'The Affluent Society' (first published 1958). Pelican Book Paperback. Page 149, 153.

[2] Why we need to lie to ourselves about the state of the economy

Satyajit Das August 28, 2015

http://www.smh.com.au/comment/satyajit-das-column-20150825-gj7bcy.html

[3] World Per Capita Oil Consumption 1965 – 2009 (pdf/3 pages) by John H. Walsh.

http://pages.ca.inter.net/~jhwalsh/oilcapv3pages.pdf

[4] Figure 2 in Alan Cole's article: 'Losing the Future: The Decline of U.S. Saving and Investment' dated October 01, 2014, shows that investment rose above savings earlier than 1980. This rise in 'investment' funds was likely the result of the 9 fold increase in oil prices that occurred in the 1970s.

http://taxfoundation.org/article/losing-future-decline-us-saving-and-investment

[5] The new world order and the failure of globalisation

Alan Freeman (2002): The new world order and the failure of globalisation. Unpublished.

The new political geography of poverty. University of Greenwich

http://mpra.ub.uni-muenchen.de/2652/

Posted on 10th April 2007

[6] The real problems with $50 oil

By Henry C K Liu May 26, 2005

http://www.atimes.com/atimes/Global_Economy/GE26Dj02.html

[7] 'Sleepers Wake - Technology and the future of work', Barry Jones. Oxford University Press 1982.

[8] Charles Derber in his 1998 book 'Corporation Nation' quotes former US President Rutherford B Hayes about the 'Gilded Age' he lived in: "This is government of the people, by the people and for the people no longer. It is a government of corporations, by corporations and for corporations." Derber observes of our contemporary reality "[Corporations "constant dialogue] is more than idle chatter: their intricate network of connections constitutes what is, in essence, a new worldwide corporate web." Page 18.

Wednesday, February 18, 2015

How Legitimate is Greek Debt?

Latest update: 19th July 2015

[Image above is of the chin of the current head of the International Monetary Fund]

The Greek government is struggling to pay the debts it took on to bail out the country's private banks. The newly elected government, headed by Prime Minister Alexis Tsipras, has been opposing IMF, EC and ECB 'bailout' conditions on humanitarian grounds. On 5th July 2015, a large majority (61%) of Greek citizens who voted on a referendum on this issues opted to reject the bailout terms offered by this 'Troika'.

Demands placed on the Greek government included implementing a higher tax on goods and services, forcing 100% advance tax payments on corporations and generally increasing taxes across the board. Social welfare entitlements were to be limited and payments decreased. More effective measures were required to target tax evasion. The electricity company, the airport and shipping ports were to be privatised, efforts were required to weaken the collective bargaining of workers And so on. [1]

However, only days after the Greek people took Tsipras' lead to reject such imposed austerity in the referendum, the Greek Prime Minister took a U turn and signed up such measures after all. [2]

“Alexis Tsipras at some point decided that his government, our government, was at gunpoint. We were given a choice between being executed and capitulating and he decided that capitulation was the optimal strategy."Said Greece's former Finance Minister, Yaris Varoufakis. [3]About one third of Tsipras party have voted against the austerity measures. They want Greece to reintroduce it's national currency, the drachma. [4]

But what made Greece such a debt junkie in the first instance? Does Greece suffer from a fundamental lack of economic capacity? Is Greece exceptional with regard to her inability to repay? Have lenders inappropriately pushed loans? Have the recipients borrowed beyond their means?

In 2012, Greece's government had the largest sovereign debt default in history and on 30th June, 2015, Greece became the first developed country to fail to make an IMF loan repayment.[5]

Events are unfolding that reveal that most of Greece's struggle and dilemma is revealed to be symptomatic of a much wider and global, form of economic and financial failure.

The former Greek finance minister, Yanis Varoufakis resigned months after taking office in early 2015. He has pleaded with his nation's creditors that Greece is simply not capable of paying back the debt. He is alarmed that the so-called 'Troika' of the IMF, the European Commission and the European Central Bank are not 'bailing out' Greece, as they publicly assert. Rather, Greece is being loaded with more debt. Greece says Varoufakis, is "caught up in an existentialist crisis caused by its membership of a problematic currency union."[6]

Varoufakis explains the dynamics of Greece's extraordinary bailout process:

At the same time, Greece is being weakened in its capacity to repay this rather dubious form of debt by demands for greater and greater fiscal austerity. Varoufakis calls it 'ponzi austerity' where every effort is made to give the public the illusion that the debt problem is being dealt with whilst the reality is that this problem has actually worsened.

- "Step 1: Banks issued private bonds which they did not intend to sell to anyone

- Step 2: Banks got (under a veil of ignorance and a conspiracy of silence) the Greek state to guarantee these bonds – without seeking parliamentary approval, without the troika’s official approval, without even informing the electorates in Greece or in Germany or anywhere else of this massive increase in the Greek state’s effective liabilities

- Step 3: Banks then posted these bonds with the ECB in exchange of instant cash." [7]

"When bankrupt a large loan does not help, as long as the loan is not preceded by a debt write off. And, when the large loan, without an upfront haircut, comes with the condition of reducing your income (for this is what austerity does), then it is a predatory, toxic, ridiculously irrational policy."[8]The vast portion of the capital said to have been passed to Greece is, Varoufakis said, being used to prop up large German and French banks in particular.

The crisis in Greece began to climax shortly after the beginning of a global financial crisis which was officially declared to have begun in 2008. Before that most citizens in the richest industrial countries might have believed we were still enjoying one of history's longest and greatest economic booms. For instance, in 2005 the US Federal Reserve chairman Ben Bernanke spoke of a 'global savings glut'.

In actuality a form of 'ponzi growth' was taking place in the world economy.

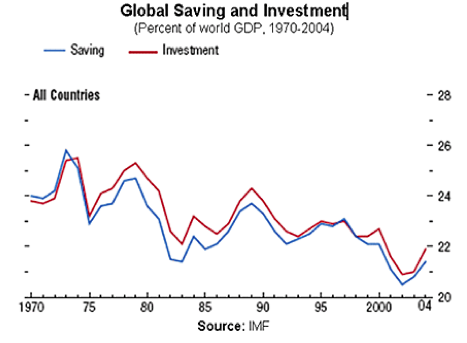

"...we observe is that world savings rates have actually declined from the 1970’s to the present time [See above chart]. So the crude notion of a savings glut doesn’t seem to reconcile the data with the theory because if there is a savings glut now then there would have been a much higher savings glut in the 1970’s, and yet real and nominal rates were high in the late 1970’s and extremely high in the early 1980’s. Ironically, the savings glut concept, global aggregate demand shortfall, insufficient consumption discussions dominated the economic discussions of the 1930’s." [9]

A senior Australian Reserve Bank official observing this dynamic said it was "akin to the Dotcom Crash "… and were it to stop, a sharp fall in the US dollar and a bond market sell-off would occur, pushing up US and world interest rates in a global economic crash. This would hit US economic growth and thereby cut Chinese exports of manufactured goods to the American market (undermining the engine of global growth)." [10]

Major trade imbalances were being compensated for by equal and opposite capital imbalances. The surplus countries (Japan, Germany, China...) must finance the deficit country (the US, Greece, Ireland, Portugal, Spain...) and this financing maintains its internal demand and the external demand of the surplus country. [11] Stability is maintained as long as household income in the deficit country parallels or exceeds household acquisition of debt. In the US household debt began to outstrip earnings from the late 1990s. [12]

When international lenders begin to fear the repayments of debt may not be realised, or for other reasons, capital flows out of the fragile periphery countries and throws them into economic turmoil. This is how the Greek finance minister described the unravelling in Greece once the global financial crisis commenced:

"...The reason for our insolvency was simple: The Eurozone was incapable of absorbing the shockwaves of the 2008 global earthquake. Once the capital inflows that had flooded the Periphery went out like a vicious tide, they left behind nothing but weedy posts and marooned public and private sectors. Unable to reduce the international value of our countries’ debts and banking losses through currency depreciation, with states that lacked a central bank to have their back, and a central back without a state to have its back, Europe’s mountain of debts was bound to rise while incomes took a hit. The definition of bankruptcy writ large." [13]

...

.... to be continued...

REFERENCES and NOTES:

[1] Table 1. Greece: Prior Actions

Policy: Actions to be taken in consultation with EC/ECB/IMF staff

http://europa.eu/rapid/attachment/IP-15-5270/en/List%20of%20prior%20actions%20-%20version%20of%2026%20June%2020%2000.pdf

[2] Greek bailout: Europe strikes deal after marathon talks

Mark Thompson. 12th July 2015

http://money.cnn.com/2015/07/12/news/economy/greece-bailout-europe-conditions/

[3] Greek debt crisis: reforms will fail, says ex-finance minister Yanis Varoufakis

Jamie Grierson and Helena Smith

Sunday 19 July 2015 00.17 AEST

http://www.theguardian.com/world/2015/jul/18/greece-debt-crisis-reforms-fail-yanis-varoufakis

[4] Says Anna Asimakopoulou, an MP with the conservative New Democracy party in Greece.

Source: Now a deal has been done, what lies ahead for the Greek economy? Helena Smith in Athens. The Observer, 19th July 2015.

http://www.theguardian.com/world/2015/jul/18/greece-eu-debt-deal-what-lies-ahead

[5] Greece fails to make IMF payment as bailout expires

Elena Becatoros and Raf Casert, The Associated Press

Published Tuesday, June 30, 2015 5:02AM EDT

http://www.ctvnews.ca/business/greece-fails-to-make-imf-payment-as-bailout-expires-1.2446852

[6] Yanis Varoufakis: Italy’s collapse will change the Austerian way in Europe

Interview by Jorge Nascimento Rodrigues. 25th June 2013

http://janelanaweb.com/novidades/yanis-varoufakis-italys-collapse-will-change-the-austerian-way-in-europe/

[7] How the Greek Banks Secured an Additional, Hidden €41 billion Bailout from European taxpayers

Posted on May 11, 2014 by yanisv

Yanis Varoufakis – Thoughts for the post 2008 world

http://yanisvaroufakis.eu/2014/05/11/how-the-greek-banks-secured-an-additional-hidden-e41-billion-bailout-from-european-taxpayers/

[8] Yanis Varoufakis: Italy’s collapse will change the Austerian way in Europe

Interview by Jorge Nascimento Rodrigues. 25th June 2013

http://janelanaweb.com/novidades/yanis-varoufakis-italys-collapse-will-change-the-austerian-way-in-europe/

[9] Spotlight, February 2006.Chris Dialynas Discusses the Causes and Implications of Low Interest Rates and the Yield Curve Conundrum. Chris P. Dialynas, Managing Director, Portfolio Manager and Senior Member of PIMCO’s Investment Strategy Group

http://australia.pimco.com/LeftNav/PIMCO+Group+Spotlight/2006/Dialynas+Spotlight+Feb+2006.htm

[10]

The Generation Project: 2000-2005

© Mark Verma 2005

http://members.iinet.net.au/~verma/p_generation11.html

[11] If this financing is by buying assets, the surplus country gains the “property” of the deficit country; and if the financing is by loans, the surplus country gains “sovereignty” over the deficit country.

[12] Guest Post: Our Era’s Definitive Dynamic: Diminishing Returns

[11] If this financing is by buying assets, the surplus country gains the “property” of the deficit country; and if the financing is by loans, the surplus country gains “sovereignty” over the deficit country.

[12] Guest Post: Our Era’s Definitive Dynamic: Diminishing Returns

Submitted

by Tyler Durden on

11/09/2013 20:59 -0400

Submitted

by Charles Hugh-Smith via Peak Prosperity

http://www.zerohedge.com/news/2013-11-09/guest-post-our-era’s-definitive-dynamic-diminishing-returns

[13] BEING GREEK AND AN ECONOMIST WHILE GREECE IS BURNING!

An intimate account of a peculiar tragedy. Yanis Varoufakis, November 2013

https://varoufakis.files.wordpress.com/2013/11/mgsa-talk-nov-2013.pdf

[13] BEING GREEK AND AN ECONOMIST WHILE GREECE IS BURNING!

An intimate account of a peculiar tragedy. Yanis Varoufakis, November 2013

https://varoufakis.files.wordpress.com/2013/11/mgsa-talk-nov-2013.pdf

Saturday, February 15, 2014

Nelder: Peak Oil Isn't Dead

Chris Nelder's article: 'Peak oil isn't dead; it just smells that way' is a helpful and relatively recent update on the peak oil discussion.

Since at least 2005 there has been a massive increase in the financial investment to fund production in oil. This has been paid for by higher prices for fuel. The result, however, has been merely a rough global plateau of production in crude oil since that time. Global demand keeps rising as population and expectations rise also. So other forms of liquid fuel (such as ethanol) have been employed to supplement supply. However the energy intensity and the energy return on energy invested (EROEI) of these alternative fuels is significantly lower than for crude oil.

The world, in summation, already has an energy-related transport crisis in the respect that the fuel we use to run our vehicles is now much, much more expensive than it was compared to a decade ago and the prices continue to rise at a faster rate than our incomes do. The result can only be reflected in a lower general standard of living without changes in lifestyle.

The Jilted and the Landless

Britain has gone to pot and its the fault of the

baby boomer generation says two media journalists (Ed Howker from 'The

Spectator' magazine and Shiv Malik from the 'Sunday Times' and 'Prospect'

magazine). If it wasn't for the short-term horizons and rampant

consumerism of the British people from my generation then those young adults of

today - those born from 1979 and later - would be enjoying a good supply of

cheaper, better quality housing, as well as jobs that paid a reasonable

remuneration and were also secure. It is claimed that the denial of those

things has led to their "postponement of adulthood" and a lifestyle

of poverty and aimlessness. [1]

The crisis in Britain, as described in Malik and

Howker's book 'Jilted Generation' is particularly relevant because it is also

mirrored in most so-called 'first-world' nations today. I have no real

argument against their description of the predicament of the post 1979ers but a

lot of the analysis of this book lacks depth and historical understanding.

It may be quite normal for young adults to pin the

blame for things gone wrong on the generation who came before and I can relate

to that. Who would argue against the proposition that there

aren't, indeed, huge numbers of baby boomers who should be accepting a great

deal of responsibility for the dire situation that our offspring find

themselves in now. Many boomers have wielded high levels of decision-making

power in our political and social institutions.

Howker and Malik, however, fail to describe the

global trends and forces that acted upon the their parents' generation. In

addition, barely recognise the extent to which many baby boomers very actively engaged in a

rebellious backlash against the very unsustainable materialistic lifestyle

and attitudes that these same authors rage against now. There did exist,

after all in the 1960s and 1970s, a notable counter-culture stratum of society,

and it wasn't ever all about drugs and other politically naive distractions.

One of the most fundamental aspects of the youth counter-culture, for

instance, was the 'Back to the Land Movement'. [2] In the 1960s and 1970s

young people flocked to rural areas with the aim of creating a simpler, better

way of existing free from many of the constraints of what they saw as a

dysfunctional and (ultimately) unsustainable mainstream society. Though

'back to the land movements' have existed long in time

"...what made the later phenomenon of the

1960s and 1970s especially significant was that the rural-relocation trend was

sizable enough that it was identified in the American demographic

statistics..."[2]

A strong belief existed in the 1970s that a

movement onto rural land would result in lower housing costs, better living

standards, improved health, and general wellbeing. One would engage

directly in organic agriculture and home building and, through these actions,

earth-centred lifestyles and communities would become self-sustaining.

The hope existed that a new culture would emerge and spread quickly and

widely enough to avoid a 'limits to growth' catastrophe in the new millennium.

Needless to say, that dream didn't pan out.

Time and opportunity constraints mean that the full

explanation of political and social trends that begin to explain the failure of

counter-culture (such as concentration of power, consumerisation of politics,

etc) cannot be explored here. However, the issues that relate to the

availability/cost of land are, perhaps, where it might be the most fruitful for

an inquirer to explore reasons for the degeneration in civil life and severe

depletion of common wealth (in the 'rich' industrialised nations at least).

Land, the authors of 'Jilted Generation'

acknowledge, is "the major cost in the purchase of a home" [3].

Lack of land (in terms of decentralised ownership) may be the very

reason why 93% of homes built in London between 2000 and 2010 have been

"poky one and two-bedroom flats." [4] The fact that less than

one percent of Britain's population own it entire base of farmland [5] might

explain why a 'back to the land movement' cannot exist there.

For surely land is the only form of genuine

cultural escape when we find ourselves living out an empty materialism -

expressed as 'consumerism' - in a deprived 'dollars-and-cents' reality.

Brenda Rosser

REFERENCES:

Picture: Drop City was an artists' community that formed in southern Colorado in 1965. Abandoned by the early 1970s, it became known as the first rural "hippie commune".

Picture: Drop City was an artists' community that formed in southern Colorado in 1965. Abandoned by the early 1970s, it became known as the first rural "hippie commune".

[1] 'Jilted Generation - How Britain has

Bankrupted its Youth' by Ed Howker and Shiv Malik. Icon Books Ltd,

Omnibus Business Centre. Published 2010. ISBN: 978-184831-198-5

[2] Back-to-the-land movement, Wikipedia

http://en.wikipedia.org/wiki/Back-to-the-land_movement

[3] Page 41: 'Jilted Generation -

How Britain has Bankrupted its Youth' by Ed Howker and Shiv Malik. Icon

Books Ltd, Omnibus Business Centre. Published 2010. ISBN:

978-184831-198-5

[4] Page 213: 'Jilted Generation

- How Britain has Bankrupted its Youth' by Ed Howker and Shiv Malik. Icon

Books Ltd, Omnibus Business Centre. Published 2010. ISBN:

978-184831-198-5

[5] Reclaim the Fields

Ed Hamer discovers a European youth movement taking

action on the issue of access to agricultural land.

http://www.thelandmagazine.org.uk/articles/reclaim-fields

Subscribe to:

Comments (Atom)